Why systematic withdrawal plans in MF work best for retirees

Systematic withdrawal plan allows unitholders to withdraw money at regular intervals. A Moneycontrol analysis of MC30 debt and equity funds show that 6-8% can be ideally withdrawn every month without depleting the corpus, if you stay invested for 10 years

It is common knowledge that Systematic Investment plan (SIP) is a popular tool to invest in mutual fund schemes. But did you know that Systematic Withdrawal Plan (SWP) is just as efficient to get regular income in your hands? In an SWP, you choose the withdrawal amount, the frequency and the duration according to your needs. Money comes in your bank account, automatically. SWP is an efficient tool to earn regular income after retirement. If you invest regularly and accumulate a tidy corpus in the initial years leading up to your retirement, the SWP facility can be successfully triggered upon your retirement. Retirees can use their retirement savings, gratuity, corpus, etc., and opt for an SWP by choosing a suitable mutual fund schemes. You can consider the MC30, a curated list of 30 investment worthy mutual funds across equity and fixed income categories, for your SWP requirement.

2/14

While the SWP enables you to receive a fixed flow of income regularly, the remaining investment in the schemes are kept to grow over period which will eventually help increasing your corpus size. While an SIP averages out the cost of purchase, SWP averages out the cost of withdrawals. Remember: There is no guarantee that your capital will stay intact forever. If your rate of withdrawal is greater than the rate at which your scheme grows, you might end up dipping in your capital. hence, for conservative investors, make sure your retirement basket of investments include Fixed Deposits and Senior Citizens Savings Schemes and use SWP in mutual funds as an add-on.

3/14

How much should you withdraw using SWP? Vidya Bala, Co-founder, PrimeInvestor.in says, “For SWPs, a large corpus, a realistic return assumption and a rate of withdrawal lower than the return assumed would be an optimal way to get monthly cashflows”. If you do not want to deplete your corpus, then the rate of withdrawal should be lower than the average return potential of the investment products Bala adds. Experts advise 4%-6% per annum should be the annual withdrawal rate if you do not want to erode your capital amount. Our back of the envelope calculation shows that 6% per annum is an optimum withdrawal rate in short duration funds while it is 8% in hybrid and equity oriented schemes for the tenure of 10-years (see below slides). Note, inflation has not been taken into account in the study. Equity oriented schemes can be suitable for SWP if you have a stomach for high risk appetite and longer withdrawal duration. More importantly, market conditions matter while deploying lumpsum money in equity funds. Consult your financial advisor before investing your hard earned money in equity funds. If you do not mind depleting capital, then your withdrawal rate can be based on your requirement.

Taxation SWP redemption is as per the first-in-first-out (FIFO) method wherein units bought first are assumed to be redeemed first. Equity: 10% of long-term capital gain tax (excess of Rs 1 lakh) if held for more than a year. 15% of short-term capital gain tax held for less than one year. Non-equity including debt funds: Taxed as per investor’s slab rate (for the investment made on or after April 1, 2023)

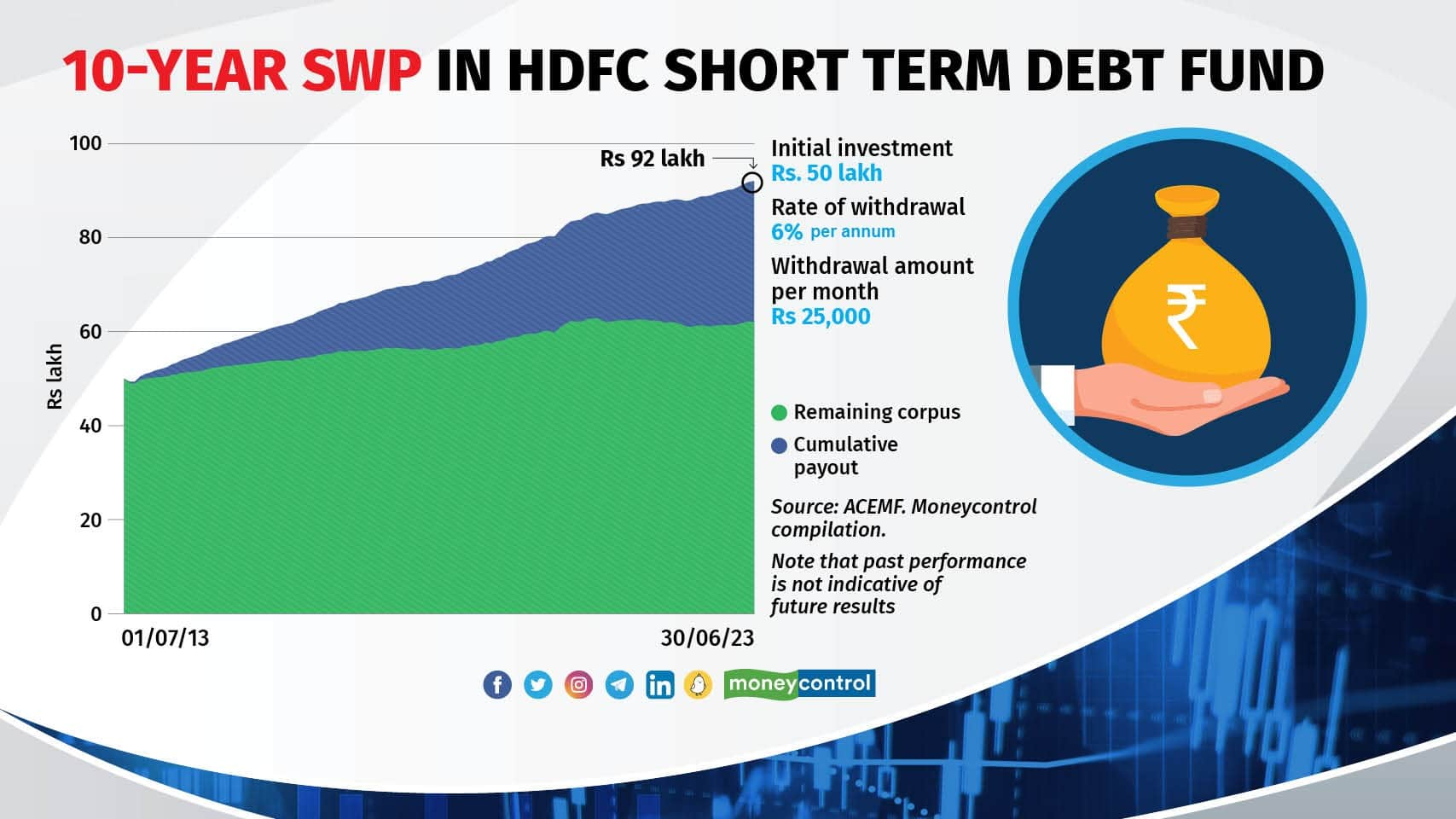

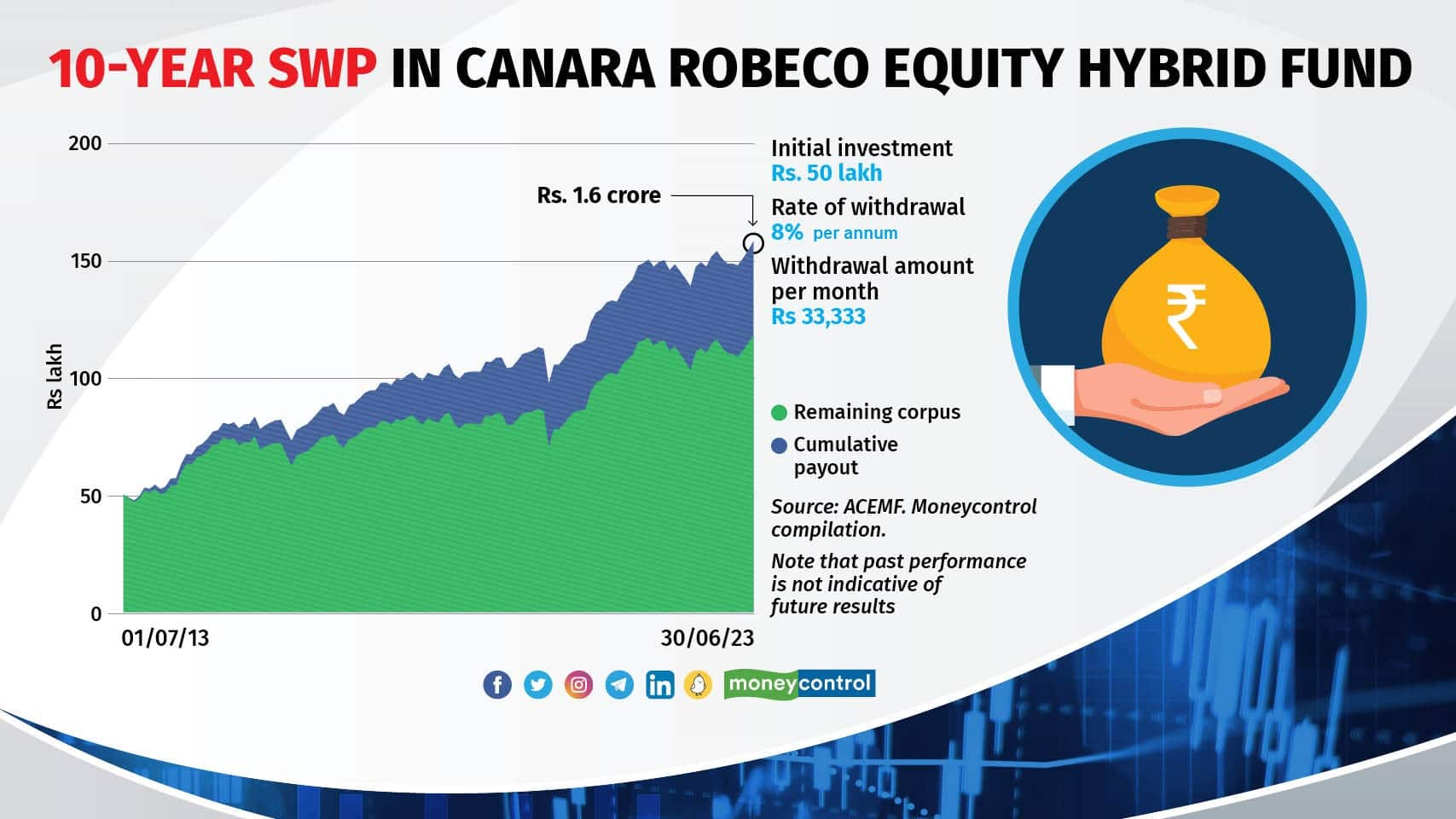

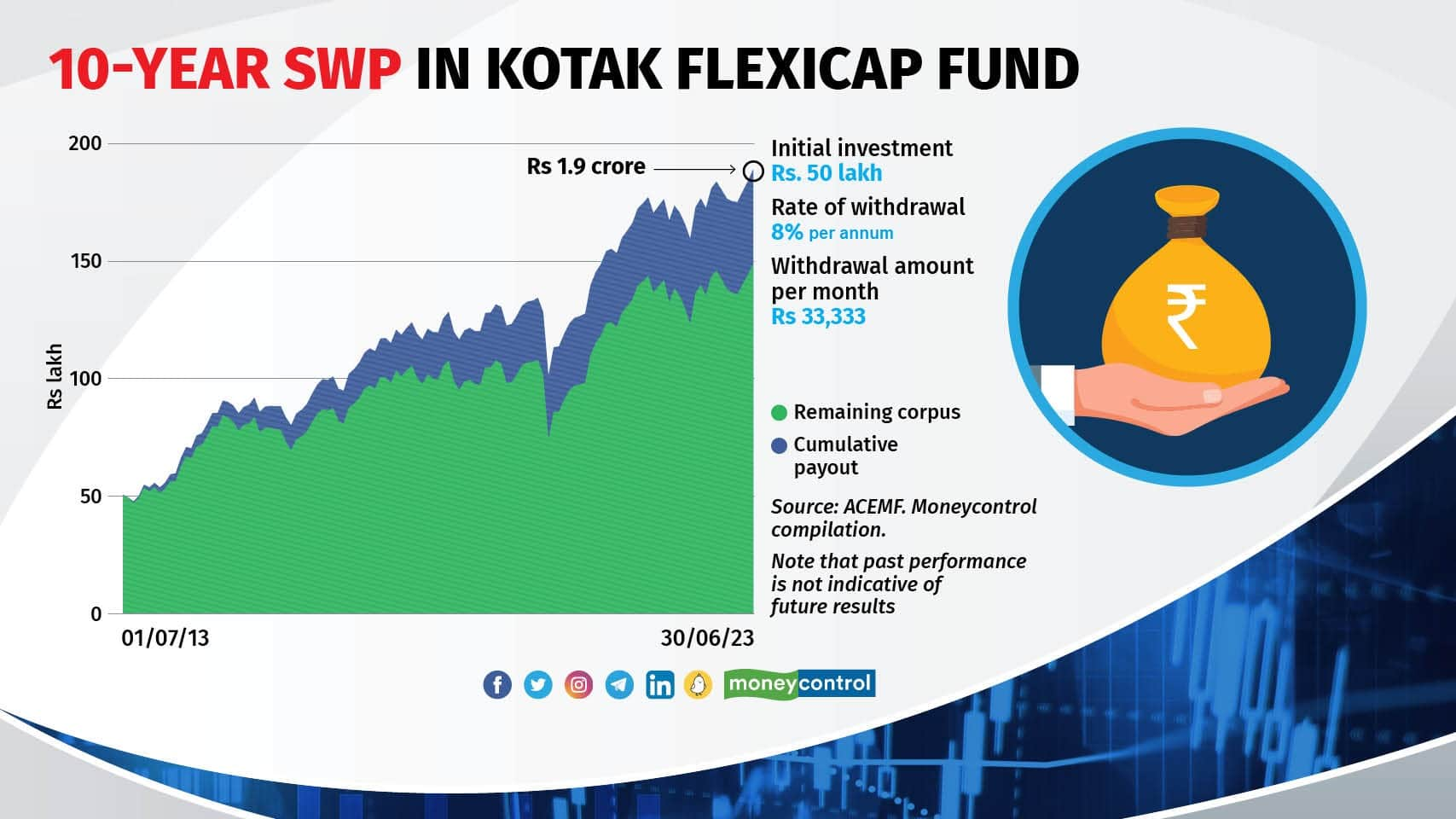

In below charts, we computed SWP withdrawal over the last 10 years for the initial investment amount of Rs. 50 lakh made in the schemes under major categories that part of MC30 basket. Largecap, flexicap, aggressive hybrid and short duration funds are considered for the study. Annual withdrawal rate of six percent (Rs 25,000 as monthly withdrawal amount) is applied for short duration schemes while it was eight percent (Rs. 33,333 as monthly withdrawal amount) for equity and aggressive hybrid funds.

is a popular tool to invest in mutual fund schemes. But did you know that Systematic Withdrawal Plan (SWP) is just as efficient to get regular income in your hands? In an SWP, you choose the withdrawal amount, the frequency and the duration according to your needs. Money comes in your bank account, automatically. SWP is an efficient tool to earn regular income after retirement. If you invest regularly and accumulate a tidy corpus in the initial years leading up to your retirement, the SWP facility can be successfully triggered upon your retirement. Retirees can use their retirement savings, gratuity, corpus, etc., and opt for an SWP by choosing a suitable mutual fund schemes. You can consider the MC30, a curated list of 30 investment worthy mutual funds across equity and fixed income categories, for your SWP requirement.")

: 7.4%")

: 7.7%")

: 14%")

: 16.8%")

: 18.7%")